First, let's look at what Lending Club says I earn:

If you are not familiar with Lending Club's dashboard, let me use this time to explain this. You can see on the left that "primary notes" and "traded notes" are grey'd out. This means that my account contains both notes I purchased new and kept, as well as notes I either purchased from or sold to another user (I've done both). That 10.07% figure assumes that all notes not currently in default will pay the full amount owed on the date owed, an assumption that everyone knows is not true. Further, it does not take into account that you always have money in your account that is not earning interest. If you look at the chart above, at the time that screenshot was taken, I had $1.50 that was totally un-invested and $225.00 that was committed to notes but not yet invested, meaning that it was earning no interest.

On the right side of the chart you can see that during my time with Lending Club I have purchased 1330 notes, or parts of loans. Of those, 9 are still being processed (and aren't earning me anything); 971 are current and paying, 8 are in grace period (less than 15 days late), 4 are between 16 and 30 days late, 32 are over 30 days late and 55 have been charged off as worthless (though Lending Club does sell them to a debt collector and will credit your account a little when that happens).

As I said, the first figure assumes that all borrowers will pay as promised, and that everyone knows that isn't going to happen. This second figure shows Lending Club's estimate of what is more likely to be true. Their experience has shown that 10% of the value of notes which enter grace period is lost. Obviously, that is on an aggregate basis, not an individual one since most end up paying, just late but those few that don't are the reason for the drop. Based on the number of late notes currently in my portfolio, Lending Club estimates the real value of my account to be $557.80 less than shown in the first figure and estimates that my rate of return is 7.49% rather than 10.07%. However, even that figure is inflated as it does not take into account the cash drag--the money in my account that is not earning anything. Today's figure of $225 is pretty average; some days it is more (like if several people decide to pay off loans) and some days it is less.

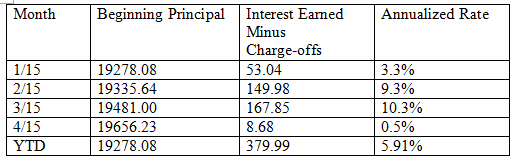

So, what am I really earning, and how do I compute it? Well, one way that works well, if you are not adding principal to the account, is looking at the principal at the beginning of the month and the amount of interest earned that month, minus what you lost to defaults, and annualize the results. Lending Club sends out statements monthly, using the actual rather than adjusted figures. Here are mine for the last few months:

If you are adding or withdrawing principal, the XIRR method is considered the most accurate. You can use Excel to compute this (but don't ask me how) or you can use this online calculator. Using the adjusted values, it shows my returns to be 6.75%; using unadjusted values, my returns are 9.02%. In either case, this far exceeds my stock market returns during the same time. My account has grown from $17,050 to over $19,000. Why are the XIRR results so much higher than annualizing monthly returns as above? Because the first few months the returns are artificially high as defaults have not started to hit yet. For example I have one portfolio in which I keep all the notes I have purchased this year (2016). As of today, May 8, all are current; none are late. As these notes age, and some quit paying my overall return on that group of notes will fall.

One thing Lending Club allows you to do is to divide your notes into "portfolios" and to therefore track different portfolios. My next post will talk about my Lending Club portfolios.

I haven't been able to figure out what time period Lending Club uses to compute Net Annualized Returns. I compute trailing-12-months XIRR in Excel and it's always lower than what Lending Club shows.

ReplyDeleteLending Club computes on a per-note basis and does not account for cash drag

Delete